The truth about money

The truth about money is going to surprise you.

It will probably be more of a surprise based on the fact I’m a financial adviser.

The thing is, I can’t really cover The Truth About Money in just one blog. Therefore, I plan to discuss the elements about the truth about money over the next few blogs to allow you to digest the information in bite-size chunks.

My next one will be titled “How to become a millionaire?”

But, let’s not delay it any further. You want to know what The Truth About Money is don’t you?

Truth #1

The first truth about money is that it should be SPENT!

Yes, that’s right. It should be spent.

Money is no good to anyone unless it’s used!

Money is a means of exchange for value for goods and services. It holds no purpose on its own.

The only question really is when do you spend it?

Do you spend it now or in the future?

Are you spending it for yourself, or for someone else?

If you’re going to spend it now – great! Go and enjoy it!

However, if you plan to spend it in the future, this is where you need to consider the best home for your money until the time you plan to spend it.

Money does nothing, neither for yourself or the economy, by sitting under your mattress.

Unfortunately, since the Financial Crisis in 2008 interest rates have been at historic lows and any money sat in a savings account has probably done little better than sit under the mattress in the last 10 years.

However, frustrated you may be with the lack of interest earned the truth is even worse.

Truth #2

The Second Truth About Money: Your savings are worth less now than they were then!

Let me explain.

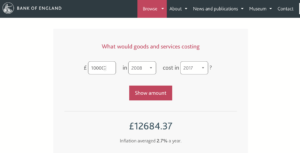

If you had £10,000 in a savings account in 2008, it has lost £2,684 in buying power since then, with inflation averaging 2.7% over the last 10 years.

The below is a screen shot from the Bank of England Inflation Calculator.

Feel free to visit yourself and see the impact of inflation on different figures over time.

Let me put the impact of inflation another way.

If your savings account has been paying you 0.5%, the impact of inflation has reduced this to -2.2% (0.5% interest earned minus the cost of living increasing 2.7%).

This assumes no tax has been deducted from the interest earned. The actual amount could very well be less than this.

Your Bucket List

My question to you: What is on that bucket list?

What are you planning to spend your money on?

Is the price likely to be more or less than it is now?

I imagine it is likely to be more, and therefore, your money needs to grow to ensure you are not sacrificing on your plans.

Can you afford to lose 2.2% per year?

What impact does this have on your plans? Does that bucket list need to be reduced?

Of course, no-one wants to be in this position. This is where good financial advice comes in.

There are many options available to try and ensure your money is growing positively in real terms every year.

I am passionate about understanding what is important to you and what you want to do with your money?

By understanding this, it allows me to develop tailored plans to let you know the right options available to you to:

· Save tax

· Earn real rates of return

· Achieve and maintain the lifestyle you desire

I can assist by working with you to design financial plans to ensure that your money is working for you to allow you to spend it on what you want to and the time you want it, without sacrificing your plans.

If you are concerned about your savings and wish to discuss what other options might exist to achieve your Bucket List please feel free to contact me on 01536 639 007 or via email: conor@osullivanfp.co.uk